All signs are pointing to a huge spending spree by the federal government for this fourth quarter; the Omnibus bill was signed in late March, agencies have been guarded with their spending prior to its passing and now $80B has been obligated for defense and $63B for civilian agencies, the flood gates have been opened! Right?

Let’s take a quick look at the historical trends of Q4 spending and apply it to what we know about our current situation to see if you should hit the panic button if you are in the GovCon space and haven’t secured the contracts you need.

USA Spending has already done a little bit of work for us as they have found that there are in fact spikes in historical spending by the Fed over the fourth quarter of a fiscal year and “the end-of-year spikes consistently occurred across the decade, and generally followed the broad rise and fall of spending. On average, September spikes accounted for between 6-8 percent of the annual spending in a fiscal year.” The largest spending spikes occur during the final week of the final month of the Q4 (procrastinators).

(Source: USA Spending)

Now we know that there is an uptick in awards during the end of the year, but what is the Fed purchasing and what contractors are they purchasing it from? Especially relevant now with the prevalence of contract vehicles (potential foreshadow?), how does the Federal government buy these services?

Based on EZGovOpps’ analysis, over the last ten years, agencies have awarded approximately 70% of their funding prior to the final quarter. This varied by 1-2% each year. This typically leaves 30% available to federal contractors for Q4. *Note that this only relates to new awards, we did not take into account modifications to existing contracts.

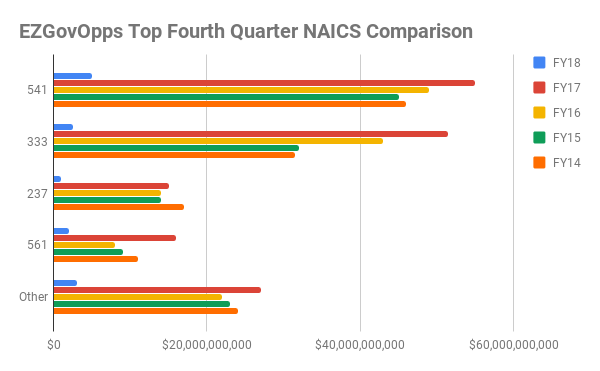

When we looked at the contractors that get the most consideration through the fourth quarter, it is no surprise that the majority of the available dollars historically goes to large businesses who take home $2 for every $1 for small businesses. We then delved into what services are being purchased most through historical Q4s; it is no huge surprise to see that most of the awards are for Professional Services (541 NAICS).

We now know that the government tends to go on a spending spree on the 11th hour of Q4, they favor large businesses and purchase mostly professional, management and administrative consulting services. Backed up by a conclusion made by USA Spending, these historic sprees are driven by new awards rather than modifications to existing contracts, which is good news to contractors angling for work.

Based on our research, these new Q4 awards are almost always single awards (as opposed to multiple awards). These awards can go through any variety of contract vehicles. Just bear in mind that the federal government will generally follow the path of least resistance, namely awards through GWACS & IDIQs utilizing purchase cards, micro-purchases and simplified acquisitions. This fiscal year, simplified acquisitions have already exceeded total spending in FY17.

So far in FY18, considering the (late) signing of the Consolidated Appropriations Act of 2018, budget caps have been increased over current spending levels and the 80:20 rule, which states DoD can’t spend more than 20 percent of its budget in the last two months of the fiscal year, has been changed to allow more flexibility at the close of the fiscal year.

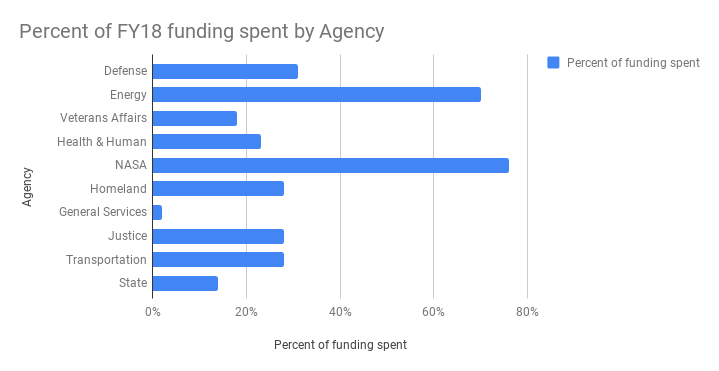

Now that we know that there is money in the agency coffers, how much money have they already used up this year? When we took a look at the top 10 agencies, we noticed that there are only two agencies that have exceeded 50% of their projected discretionary spending: NASA & DOE.

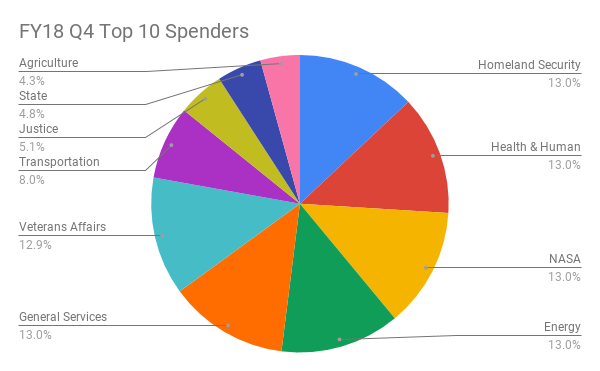

About halfway through Q4, the government has awarded in excess of $10B in funding. After seeing the largest spenders, you may notice that someone does seem to be missing. At the time of this writing, the DOD is far outside of the top 10, scratching $40M in spending. They have made some hefty awards this month, however it does take some time to process before we are able to include the new data.

The elephant in the room is that so far, FY18’s Q4 spend is the lowest Q4 spend in recent memory. This could be due to any number of variables in addition to the late signing of the Omnibus package. For example, hiring freezes, federal layoffs and more conservative spending, in general.

Where does all of this leave you, the federal contractor, right now?

Well, keep in mind that USA Spending let us know that there is a large uptick in awards through the final week of September, around 6-8% of contract spending to be a little more exact. So, there is that. There are several agencies that are far below their projected discretionary budget for FY18. The new Omnibus bill has infused funding and flexibility for agency contracting.

Based on EZGovOpps research, there are some gains to be made in the fourth quarter that can come as a result of proper planning and ensuring you are positioned to win the work. If you haven’t put in the time to reap Q4 rewards, do not fret. Based on how this quarter has been unfolding, we at EZGovOpps foresee this infusion of funds being spent in the new fiscal year. Now is the time to plan for FY19, identify the proper agencies and the best contract vehicles for your offerings.

-Braun Felder, EZGovOpps Market Intelligence